Enough raging against the machine. In the 2 weeks since Liberation Day we've seen the stated rate of tariffs change at least 5 times. Just last weekend we saw a seemingly tech-saving exclusion on chips first announced then denied then largely just dismissed as more noise. From a 4% gap higher in the futures to a tepid Monday morning rally which has now given in to the endless pressure we've seen on the Consumer plays we've seen all year.

We're approaching acceptance. There's no one walking through that door to save companies relying on the kindness/ sanity of this administration. Earlier this week I pointed to Best Buy and Nike as two companies that should go higher on a deal. Both are now trading below the Friday close, down ~30% YTD and unable to hold a bid for more than a moment:

Recession is just an economic term. It's most useful in studying periods of history after the fact in search of clues as to timing the natural ebbs and flows of what used to be called the Economic Cycle but for the last 15 years is more accurately thought of as occasional world-threatening catastrophes and the stimulus that follows.

Downturns Cull the Herd when it comes to retailers. It's the Darwinian circle of life under capitalism. Just because this downturn is being self-inflicted doesn't mean the Selection process will be less severe. Whatever you think of this being a dumb timeline, this is the world we have and we need to figure it out on the long and short side.

Walk-Aways vs Doomed

I've talked about what's working. It's a mix of mostly longer-term names and companies that are less "imperiled" and more "annoyed" by the trade war shenanigans. We've talked about untouchable "Tell" names like Nike and Best Buy. In another camp are trades I'd normally do but can't in the new reality.

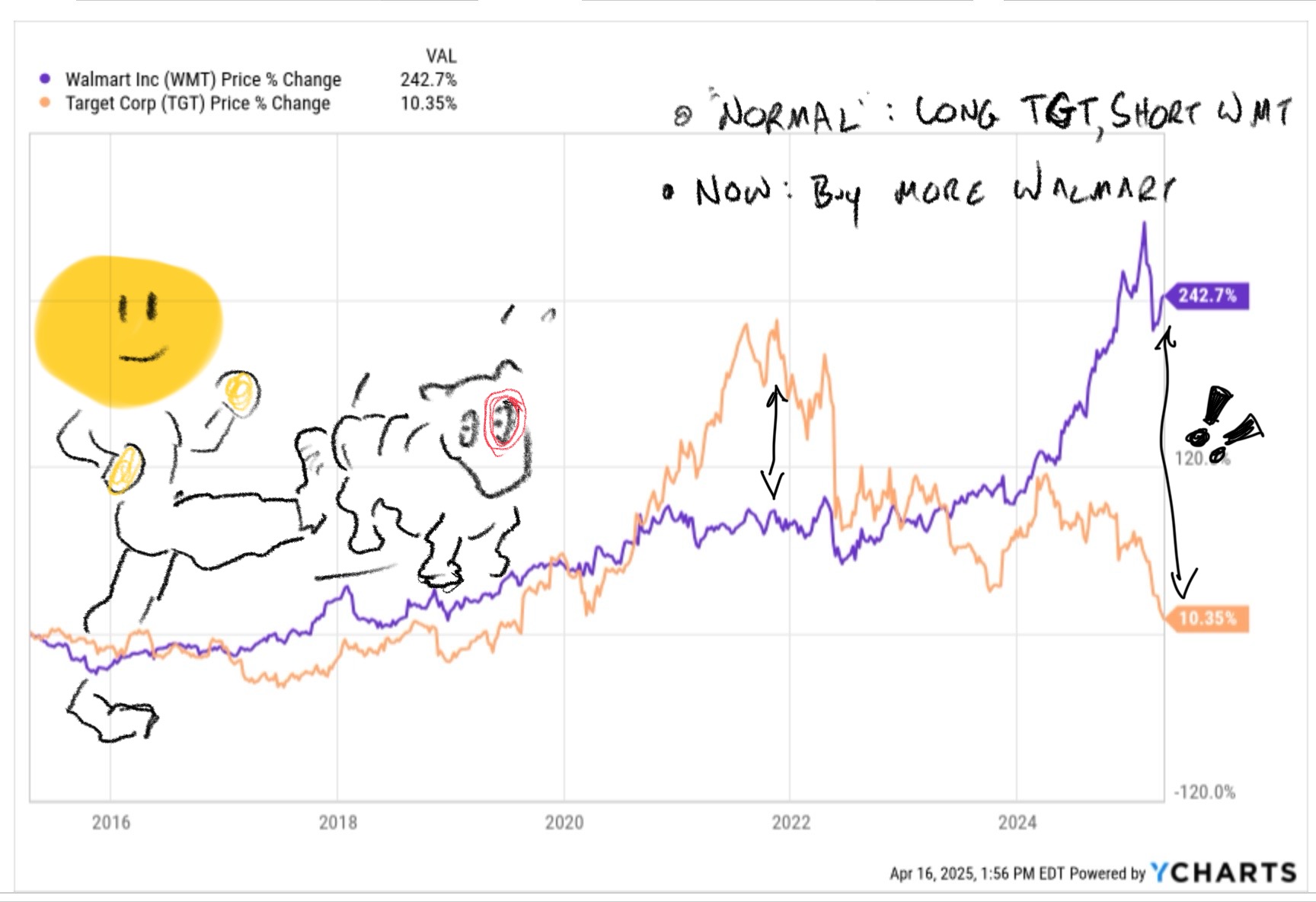

Target at less than 1/3rd the PE of Walmart shouldn't make sense. Two discounters fighting for similar (but not exactly the same) customers would, in theory, trade more less in lockstep, with a slight lead assumed for Walmart bc of better management. Not anymore. Today Goldman took down Target estimates for the year and possibly beyond, mostly for reasons we've discussed.

Here's a reason we haven't: Target has been tweaking its inventory levels with growing vigor since COVID. Remember the dock strikes last year? Probably not because they lasted about a week. Turns out Target pulled forward huge amounts of inventory in anticipation of delays, leaving the company bloated and heavy on clearance through the holidays and beyond, right into tariffs.

Goldman estimates Target has to raise prices 1-11% across the board to account for tariffs as they stand without losing margin. Here's a spoiler, Target won't be able to raise prices. What's worse, if Target yet again tried to jam through orders ahead of the tariffs, or even waited to order, assuming cooler heads would prevail, Goldman's numbers are still way too high. Target management will have to be perfect for the company to keep 25 earnings at the same level as last year. That's a lot to ask of a team that hasn't even been particularly good for half a decade.

Target is a name to short on rallies, even down this far. It's not a short, yet, but this is how retail deaths start. A few bad steps put pressure of margins. CapEx is cut to make up the difference. Service levels lag. It seems impossible to believe but Target becoming Kohl's over the next 10 years seems more likely than Target closing the gap with Walmart.

For Round Up Plus subscribers I've been working on a company in an even worse situation and how to trade it!